However, the uncertainty surrounding Social Security benefits is not universally present across all surveys. It is higher for younger people. One survey, The Survey of Economic Expectations, includes a Social Security Module. Researchers collected six points from each respondent, as well as a minimum or maximum value for subjective probability distributions. Researchers calculated uncertainties for each respondent. Results showed that younger respondents were significantly uncertain about future benefits. The Social Security system in general was also a concern for them.

Pessimism

Recent surveys reveal that Americans are not optimistic regarding their prospects of receiving Social Security benefits at retirement. Pessimism seems to be most prevalent among Americans aged 18 to 29 years. However, the general population is just as susceptible to this outlook. Four out of ten people say they expect only a small portion of their benefits in the future, while nearly half of those age thirty-four to fifty nine don't think they will ever receive any Social Security Income when they retire.

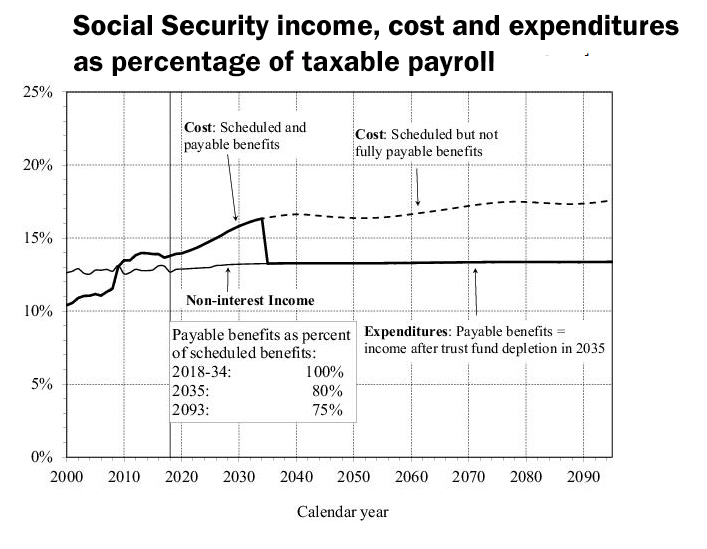

According to the recent report, Social Security will be forced to reduce benefits to those paid by payroll taxes by 2034. In that case, if Congress doesn't intervene, Social Security benefits will be cut by almost 25 percent. The government will have to raise the payroll tax in order to pay the deficit. If the trust fund was exhausted in 2035, the amount of benefits available to retirees would decline by 25 percent.

Heterogeneity

There are differences in early and late retirement. An early retiree may not have a strong work history which could reduce their chances to receive benefits. Even those who have worked hard may not be able to retire as soon as 65-year-olds. These differences in the composition of early and late retirees may be due to heterogeneity in earnings. However, the authors of the study acknowledge the contributions made by many.

The heterogeneity of net worth returns is much greater. The standard deviation of returns is 7.9%, and the range from the 90th percentile to the tenth is 16.9%. These results suggest that the returns to financial wealth are more diversified due to the use of leverage and cost of debt. The distribution of net worth returns is more uneven than the returns to net wealth. It also exhibits a greater degree of kurtosis and a longer tail to the left. Pearson's coefficient of skewness is -6.31.

Expectations and the impact of earnings

This research employs a new framework for measuring lifetime earnings and comparing them to Social Security benefits. This method uses administrative records to measure lifetime earnings and not Social Security earnings. It also includes trade-offs across several dimensions. These data are not subject to a cap like Social Security earnings. However, they do not automatically exclude uncovered earnings. As a result, these data provide a more accurate measure of lifetime earnings.

Social Security Administration (SSA), which has used CPS data since the 1970s, shows that almost 90 percent of older households have received Social Security income. This income made up between 66% and 84% of total income. Poterba (2014) used 2013 CPS statistics to calculate total income levels. He found large variations in the percentage households receiving Social Security income. It is possible to see the effect of earnings on social safety expectations in the short-term as well as the long term.

The impact of early retirement

The controversial topic of early retirement's impact on future social security benefits is not well-researched. Some research has indicated that younger people are more inclined to retire earlier. However, it remains to be seen if this will result either in fewer beneficiaries or more benefits. Researchers suggested that workers' eligibility to receive Social Security benefits should decrease to increase their ability to receive more money. But this idea isn't widely accepted.

You will also miss tax-advantaged savings opportunities by not claiming Social Security benefits as soon as you can. Additionally, early claimants will face a lower base for COLA adjustments throughout their entire retirement. This could be a problem in an era with high inflation. It is important to think about how long you will live and what health care costs you will need when you are considering your retirement options. Also, consider the impact of early retirement upon future social security.

FAQ

What Are Some Benefits to Having a Financial Planner?

A financial strategy will help you plan your future. You won't be left guessing as to what's going to happen next.

It provides peace of mind by knowing that there is a plan in case something unexpected happens.

Your financial plan will also help you manage your debt better. Knowing your debts is key to understanding how much you owe. Also, knowing what you can pay back will make it easier for you to manage your finances.

Your financial plan will also help protect your assets from being taken away.

What age should I begin wealth management?

Wealth Management should be started when you are young enough that you can enjoy the fruits of it, but not too young that reality is lost.

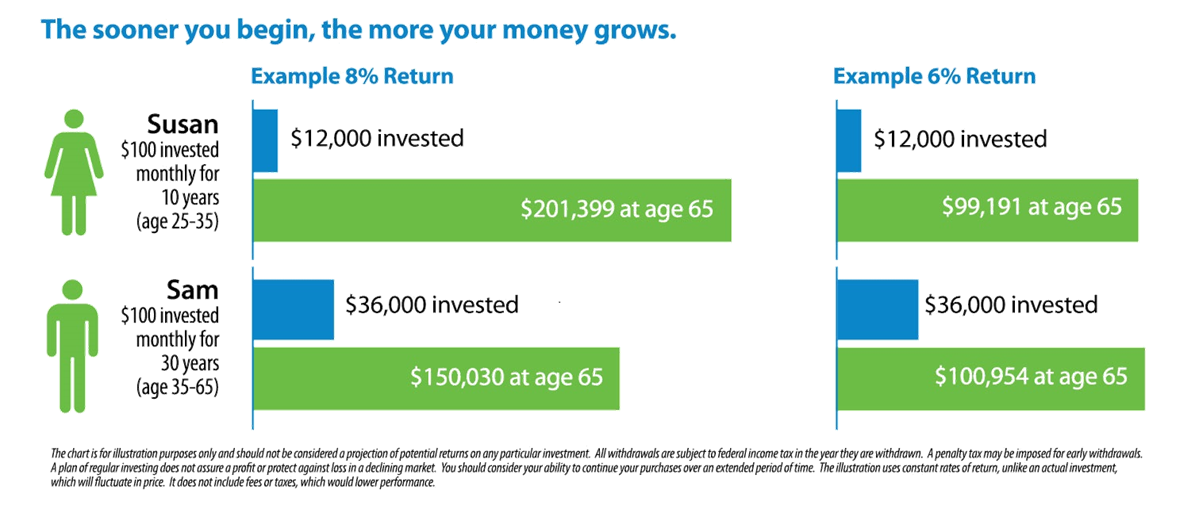

The sooner you begin investing, the more money you'll make over the course of your life.

If you are thinking of having children, it may be a good idea to start early.

You could find yourself living off savings for your whole life if it is too late in life.

How to manage your wealth.

You must first take control of your financial affairs. Understanding how much you have and what it costs is key to financial freedom.

You should also know how much you're saving for retirement and what your emergency fund is.

If you do not follow this advice, you might end up spending all your savings for unplanned expenses such unexpected medical bills and car repair costs.

What is retirement planning exactly?

Retirement planning is an important part of financial planning. You can plan your retirement to ensure that you have a comfortable retirement.

Retirement planning means looking at all the options that are available to you. These include saving money for retirement, investing stocks and bonds and using life insurance.

Statistics

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

External Links

How To

How to become Wealth Advisor

If you want to build your own career in the field of investing and financial services, then you should think about becoming a wealth advisor. There are many opportunities for this profession today. It also requires a lot knowledge and skills. These are the qualities that will help you get a job. The main task of a wealth adviser is to provide advice to people who invest money and make decisions based on this advice.

To start working as a wealth adviser, you must first choose the right training course. You should be able to take courses in personal finance, tax law and investments. And after completing the course successfully, you can apply for a license to work as a wealth adviser.

Here are some tips on how to become a wealth advisor:

-

First, you must understand what a wealth adviser does.

-

You should learn all the laws concerning the securities market.

-

Learn the basics about accounting and taxes.

-

You should take practice exams after you have completed your education.

-

Final, register on the official website for the state in which you reside.

-

Get a work license

-

Send clients your business card.

-

Start working!

Wealth advisors can expect to earn between $40k-60k a year.

The location and size of the firm will impact the salary. Therefore, you need to choose the best firm based upon your experience and qualifications to increase your earning potential.

To sum up, we can say that wealth advisors play an important role in our economy. Everybody should know their rights and responsibilities. Moreover, they should know how to protect themselves from fraud and illegal activities.